Imagine a world where you can send money directly to someone without a bank, verify the authenticity of anything from diamonds to diplomas instantly, and Imagine a world where you can send money directly to someone without a bank, verify the authenticity of anything from diamonds to diplomas instantly, and create systems where trust is built into the code rather than requiring a middleman. This isn’t science fiction—it’s the world being built on blockchain technology. More than just the engine behind Bitcoin, a blockchain is a revolutionary, decentralized digital ledger that is transforming how we think about trust, transparency, and transactions in the digital age.

What is a Blockchain? A Simple Explanation

Let’s start with the absolute basics. If you strip away all the technical jargon, what is a blockchain?

At its core, a blockchain is a special kind of database. But unlike a typical database (like a SQL database or an Excel spreadsheet), which a central authority (like a company or government) controls, a blockchain is decentralized. Its records are duplicated and distributed across a vast network of computers around the world. People call these computers nodes.

Think of it as a digital ledger of transactions. Imagine a Google Doc that isn’t stored on Google’s servers, but is instead copied thousands of times across a global network of computers. When a transaction is added to this “doc,” it updates simultaneously on every single copy. This design makes the system incredibly transparent and nearly impossible to alter fraudulently.

The Digital Ledger Analogy

A classic analogy is the shared ledger book. In a traditional bank, only the bank holds the master ledger of who owns what. In a blockchain system, imagine that every participant in the network holds an identical copy of this ledger. Every time a transaction occurs (e.g., “Alice sends Bob $10”), the network announces it to all participants. The participants (nodes) verify the transaction using a consensus mechanism (like solving a complex math puzzle in Bitcoin’s case). After verification, the transaction bundles with other recent transactions into a block. This new block then cryptographically links to the previous block, forming a chain—hence the name, blockchain.

Because each block links to the one before and after it, and because changing a single record would require altering every subsequent block on every copy of the ledger across the entire network, the data becomes immutable. This means you cannot change or tamper with it.

The History of Blockchain Technology

While blockchain technology burst into public consciousness with Bitcoin in 2009, its conceptual roots go back decades. It is a brilliant fusion of several fields: cryptography, computer science, and economics.

The Cryptographic Predecessors (1980s-1990s)

The journey begins with cryptography. In the 1980s and 1990s, researchers were already laying the groundwork:

- 1982: Cryptographer David Chaum proposed a protocol for a blockchain-like system in his dissertation “Computer Systems Established, Maintained, and Trusted by Mutually Suspicious Groups.”

- 1991: Stuart Haber and W. Scott Stornetta described the first work on a cryptographically secured chain of blocks. They aimed to create a system where document timestamps could not be tampered with, using cryptographic techniques to link documents in a chain—a core principle of today’s blockchain.

- 1997: Adam Back invented Hashcash, a “proof-of-work” system to combat email spam. This same proof-of-work concept would later become the critical consensus mechanism for Bitcoin.

The Birth of Bitcoin and the Modern Blockchain (2008-2009)

The catalyst for everything we know today was the 2008 global financial crisis. On October 31, 2008, a person (or group) using the pseudonym Satoshi Nakamoto published the now-legendary whitepaper: “Bitcoin: A Peer-to-Peer Electronic Cash System.”

This paper didn’t just describe a new digital currency (Bitcoin); it described the underlying blockchain technology that would make it possible. Nakamoto solved the long-standing “double-spend problem” in digital cash—how to prevent someone from copying and spending the same digital token twice—without needing a central authority.

On January 3, 2009, Nakamoto mined the first block of the Bitcoin blockchain, known as the Genesis Block (Block 0). Embedded in this block was a cryptic message: “*The Times 03/Jan/2009 Chancellor on brink of second bailout for banks*,” a clear commentary on the instability of the traditional financial system.

The Evolution of Blockchain Beyond Currency (2013-Present)

While Bitcoin proved the concept, developers soon realized the blockchain itself was the real breakthrough.

- 2013-2014: Vitalik Buterin, a young programmer, proposed Ethereum. After its 2015 launch, Ethereum introduced smart contracts—self-executing contracts with the terms written directly into code. This transformed blockchain from a simple payment ledger into a global, decentralized computer capable of running applications (dApps).

- 2017 Onwards: The explosion of Initial Coin Offerings (ICOs), Decentralized Finance (DeFi), and Non-Fungible Tokens (NFTs) showcased the vast potential of blockchain technology beyond finance, touching art, gaming, supply chains, and identity management.

- Present Day: We now live in an era of blockchain 3.0, focusing on scalability, interoperability between different blockchains, and sustainability. A major move from energy-intensive proof-of-work to proof-of-stake mechanisms occurred when Ethereum completed “The Merge” in 2022.

What Are Blocks and Chains?

The Building Blocks of Blockchain Explained

Let’s zoom in on the actual structure. What exactly is in a block, and how does the chain work?

Anatomy of a Single Block in the Chain

Every block in a blockchain acts like a container of data. It typically contains three main elements:

- Previous Block’s Hash: This is the crucial link that forms the chain. Each block stores the unique fingerprint (hash) of the block that came before it.

- Data: This varies by blockchain. In Bitcoin, it’s the details of transactions (sender, receiver, amount). In other blockchains, it could be contract code, health records, or property deeds.

- Hash: This is the block’s own unique digital fingerprint. It’s a fixed-length string of numbers and letters generated by a cryptographic function (like SHA-256 in Bitcoin). If anything inside the block changes, even by a single character, the hash changes completely.

How the Blockchain Creates Immutability

This chaining mechanism is what makes a blockchain so secure and tamper-proof. For example, imagine a hacker tries to alter a transaction in Block 2.

- The moment they change the data in Block 2, Block 2’s hash changes completely.

- However, Block 3 still has the old previous hash stored inside it. Now, Block 3’s link to Block 2 is broken.

- To cover their tracks, the hacker must change Block 3’s “Previous Hash” field to the new one. But doing that would change Block 3’s own hash!

This creates a domino effect. The hacker would have to recalculate and change the hash of every single subsequent block all the way to the end of the chain. Furthermore, they would need to do this on over 51% of all copies of the ledger simultaneously before the network adds new, valid blocks.

Given the enormous computational power required, especially on large chains like Bitcoin or Ethereum, this attack is practically impossible. Consequently, the longer the chain, the more secure it becomes.

Types of Blockchain Networks:

Public, Private, Consortium, and Hybrid

Not all blockchains are created equal. We can classify them based on who can participate and read/write to the ledger. There are four primary types of blockchain networks:

1. Public Blockchains

These are fully decentralized and permissionless. Anyone in the world can join the network, participate in the consensus process (mining/validating), read the ledger, and make transactions.

- Characteristics: Transparent, immutable, highly secure, but can be slower and use more energy (depending on consensus).

- Examples: Bitcoin, Ethereum, Litecoin.

- Use Case: Cryptocurrencies, open decentralized applications (dApps).

2. Private Blockchains

These are centralized and permissioned. A single organization controls them, and participation is by invitation only. The controlling entity sets the rules and can override or modify transactions.

- Characteristics: Faster, more efficient, but less decentralized and secure against internal tampering.

- Examples: Hyperledger Fabric, R3 Corda (often used in business consortia).

- Use Case: Internal auditing, supply chain management within a single company.

3. Consortium (Federated) Blockchains

This type is a middle-ground. A group of organizations, not a single entity, governs it. It is partially decentralized because pre-selected nodes control the consensus process.

- Characteristics: More efficient than public blockchains, while maintaining a degree of decentralization and trust among members.

- Examples: Quorum (originally developed by J.P. Morgan), Energy Web Foundation.

- Use Case: Banking collaborations, cross-industry supply chains (e.g., a group of banks or shipping companies).

4. Hybrid Blockchains

These combine elements of both public and private blockchains. They allow organizations to set up a private, permission-based system alongside a public, permissionless system. Therefore, they can make certain data or transactions public for verification while keeping the rest confidential.

- Characteristics: Flexible, offers controlled transparency, but can be complex to set up.

- Examples: Dragonchain, XinFin.

- Use Case: Real estate (public records of ownership with private contract details), regulated markets that require some public auditability.

How Does Blockchain Work?

A Step-by-Step Process Breakdown

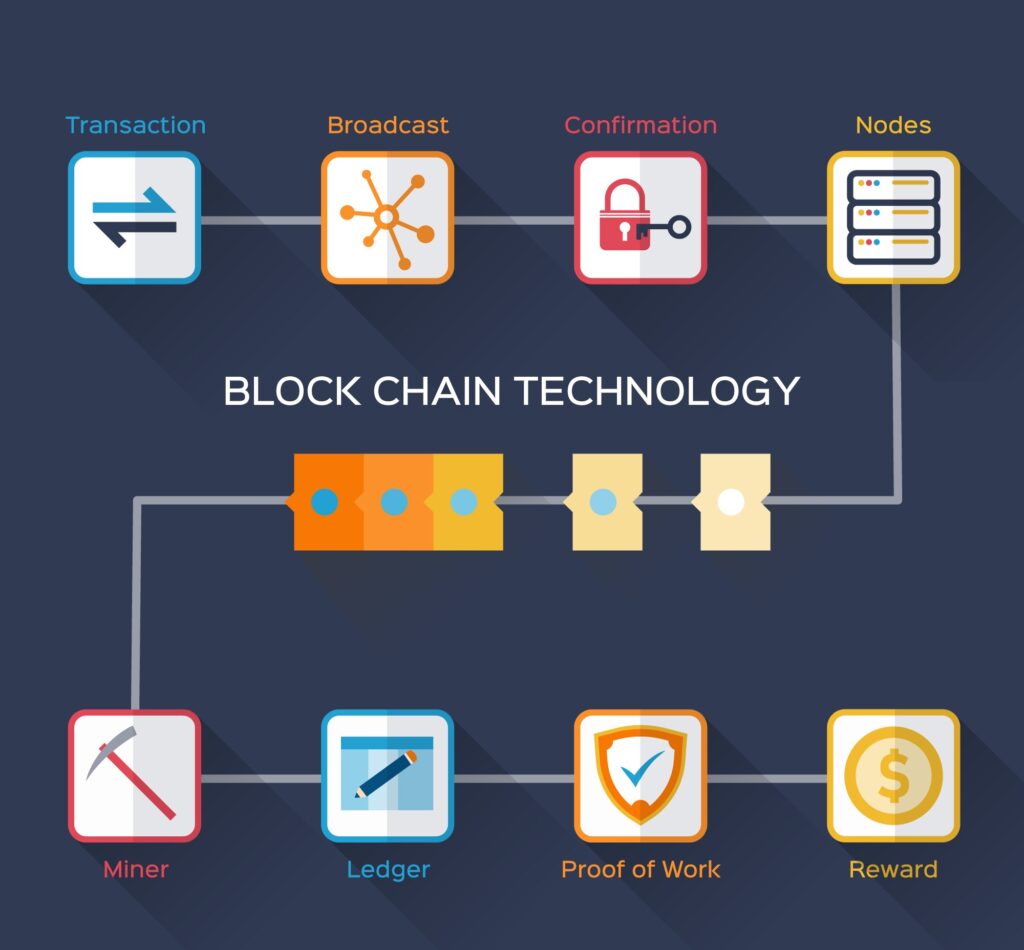

Let’s walk through the entire process from transaction to confirmed block, using a public blockchain like Bitcoin as our model.

Step 1: A Transaction is Requested

Everything starts when a user initiates a transaction—like sending cryptocurrency or executing a smart contract. The user digitally signs this transaction with their private key (like a super-secure password), proving ownership and intent.

Step 2: The Transaction Broadcasts to the P2P Network

The signed transaction broadcasts to the peer-to-peer (P2P) network of nodes (computers) located all over the world.

Step 3: Network Nodes Validate the Transaction

The network of nodes works to validate the transaction. They check several things: Is the digital signature valid? Does the sender have sufficient balance? Is the transaction format correct? The network rejects invalid transactions.

Step 4: Formation of a New Block

Validated transactions pool together into a mempool (memory pool). Special nodes called miners (in Proof-of-Work) or validators (in Proof-of-Stake) collect these transactions and assemble them into a candidate block.

Step 5: The Consensus Process – Reaching Agreement

This step is the heart of the blockchain’s trust mechanism. The network must agree that the new block is valid before adding it to the chain. Different blockchains use different consensus algorithms:

- Proof-of-Work (PoW – Bitcoin): Miners compete to solve an extremely complex cryptographic puzzle. The first to solve it adds the block and earns a reward of new bitcoin. People call this process mining.

- Proof-of-Stake (PoS – Ethereum): The network chooses validators to create a new block based on how much cryptocurrency they “stake” (lock up) as collateral. This method is more energy-efficient than PoW.

Step 6: Adding the New Block to the Chain

Once the network reaches consensus, the new block cryptographically seals (its hash generates) and appends to the existing blockchain. The network immediately broadcasts this updated chain to all participants.

Step 7: Transaction Completion

The transaction is now confirmed and permanently recorded on an immutable public ledger. As a result, the recipient receives the funds, and any smart contract executes automatically.

Why is Blockchain Important?

The Revolutionary Impact

Blockchain technology isn’t just a tech buzzword; it’s a foundational shift. Here’s why this decentralized digital ledger matters so much:

- Decentralization: Removing the Middleman

It eliminates the need for trusted third parties like banks, notaries, or platform giants to verify transactions. This reduces costs, speeds up processes, and shifts power from centralized corporations to individuals. - Transparency and Immutability: Building Trust

Every transaction records on a public ledger that anyone can inspect (in public blockchains). Once recorded, you cannot alter the data. This creates an unprecedented level of auditability and trust in systems, from food supply chains to government spending. - Enhanced Security

The distributed nature and cryptographic linking make blockchain highly resistant to hacking and fraud. There is no single point of failure. To attack it, you would need to control most of the network—a prohibitively expensive and difficult task. - Traceability and Efficiency

In complex supply chains, blockchain can track the journey of a product from origin to consumer, verifying authenticity and reducing losses from fraud. This streamlines processes and reduces paperwork and human error dramatically. - Empowering Digital Ownership (Web3)

Blockchain enables true digital ownership through NFTs and digital assets. You can own a unique piece of digital art, an in-game item, or even your social media data, verifiably and tradably, without a platform company acting as the ultimate owner. Learn more about the evolution of the decentralized web from sources like the Ethereum Foundation’s website.

The Future of Blockchain Technology: What’s Next?

The technology is still in its adolescence. Here are the key trends shaping the future of blockchain:

- Scalability Solutions: Current major blockchains can be slow and expensive. The future lies in Layer 2 solutions (like Bitcoin’s Lightning Network or Ethereum’s rollups) that process transactions off the main chain for speed, and sharding, which splits the database to increase throughput.

- Interoperability: The goal is to allow different blockchains to communicate seamlessly. Projects like Polkadot and Cosmos are creating an “Internet of Blockchains” where assets and data can flow freely between chains.

- Regulation and Institutional Adoption: Governments are creating frameworks (like the EU’s MiCA). Major institutions—from banks using CBDCs to companies like Walmart for supply chain—are integrating blockchain, driving mainstream legitimacy. Follow developments from institutions like the World Economic Forum for insights on global adoption.

- Convergence with AI and IoT: Blockchain can provide the secure, auditable data layer for Artificial Intelligence. It can also manage the massive machine-to-machine transactions in the Internet of Things (IoT), creating smarter and more autonomous systems.

- Sustainability Focus: The shift from energy-hungry Proof-of-Work to Proof-of-Stake is a major trend. Future blockchain systems will prioritize energy efficiency and carbon neutrality to be environmentally sustainable.

Conclusion: The Trust Protocol

Blockchain technology is far more than just Bitcoin or a passing trend. It represents a new paradigm for how we organize, verify, and trust information and value in a digital world. It is, in essence, a “Trust Protocol.”

While challenges around scalability, regulation, and user experience remain, the core promise is undeniable: a future with more transparent systems, reduced corruption, efficient global transactions, and individual empowerment over data and digital assets.

The journey from a cryptic whitepaper in 2008 to a technology reshaping global finance, art, and governance has been astonishing. We are still early. Just as few could predict the full impact of the internet in the 1990s, we are likely underestimating the transformative potential of blockchain technology. The building blocks are in place. The chain is being extended. The future is being written, one block at a time.

Start exploring this space today. Whether it’s understanding cryptocurrencies, exploring dApps, or considering its use for your business, engaging with blockchain is engaging with a foundational piece of our digital future.

Frequently Asked Questions (FAQ)

A blockchain is a decentralized, digital ledger that records transactions across many computers so that the record cannot be altered retroactively.

The main purpose is to enable secure, transparent, and tamper-proof record-keeping and transactions without the need for a central authority or middleman.

No, while cryptocurrency is a major application, blockchain technology has many other uses including supply chain tracking, smart contracts, digital identity, and healthcare records.

The four main types are Public (open to all), Private (controlled by one organization), Consortium (controlled by a group), and Hybrid (a mix of public and private).

Blockchain provides security through decentralization (no single point of failure), cryptography (hashes and digital signatures), and immutability (data once recorded is extremely difficult to change).

Pingback: Blockchain Technology Kya Hai? - Daily Article Hub

Pingback: Wall Street Giants Embrace Blockchain – The Future of Finance? - Daily Article Hub